Click here for a PDF version of this article

By Ben Brown, Department of Agricultural, Environmental and Development Economics, The Ohio State University – 4/17/2020

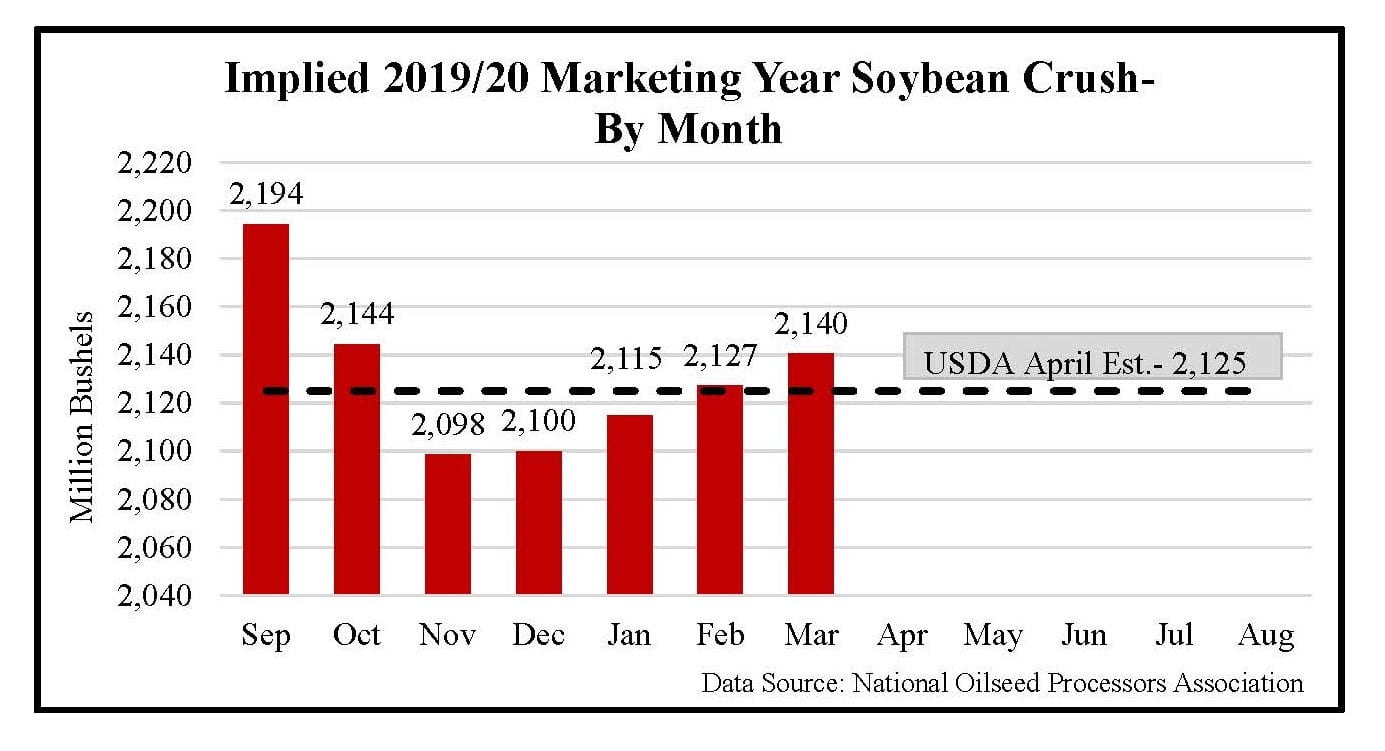

The National Oilseed Processors Association (NOPA) released their March 2020 soybean estimates on Wednesday April 15- a day that usually is not held in high regard due to US tax collections. That is until this year, when federal income tax filings could be deferred to the middle of July and NOPA released a report further solidifying one of the few bright spots in the agricultural marketplace amid COVID-19 disruptions. The report indicated that monthly soybean crushing by the organization’s 13 members who account for approximately 95% of all crushed soybeans in the US reached a new monthly crush record of 181.374 million bushels. This far exceeds any previous month and the market analyst expectation for the month of 175.163 million bushels. The March total is the first month above 180 million bushels and bested the previous record set just two months earlier by 6.211 million bushels. Soybean crush during the 2019/20 marketing year has been supported by strong domestic and international demand for soybean meal and healthy crush margins with new records being broken in four out of seven reported months- October 2019, December 2019, January 2020 and March 2020.

The USDA World Agricultural Supply and Demand Estimate (WASDE) report released April 9th increased 2019/20 marketing year crush by 20 million bushels from the February estimate to 2.125 billion bushels. This forecast would also be a record and 1.6% higher than last year’s total. Only September and November have failed to exceed the monthly values from the prior marketing year. At 181.374 million bushels reported by NOPA and a consistent rate with recent monthly USDA crush reports, the March crush report is estimated at 192.5 million bushels. That puts the seven-month cumulative total for the current marketing year at 1.265 billion bushels, roughly 60% of the April WASDE forecast. US soybean crush needs 859.5 million bushels over the remainder of the marketing year or 172 million bushels each month to meet estimates. Monthly crushing has exceeded this value every month besides September, justifying the April USDA increase. The US crushed 851 million bushels between April and August a year ago. Cumulative soybean crush is currently 9 million bushels ahead of the seasonal pace needed to reach USDA’s estimate of 2.125 billion bushels. The less than one percent advantage over seasonal adjustments implies 2.140 billion bushels. At this implied value, 2019/20 would be a 2.3% increase over 2018/19. This is not out of the question, but infrastructure capacity will be tested. US soybean crushing increased year over year by 8% in 2014/15 and 2017/18 when new infrastructure was built- the increase averaged 1.2% in other years. Current market conditions support USDA meeting and possibly exceeding the April WASDE Estimate if demand holds for the remainder of the marketing year.

Soybean meal prices have fallen in recent weeks with the rest of the agricultural commodities back to levels seen in early February on the futures market. Some cash markets have remained elevated as soybean meal demand replaces the lack of dried distillers grains in feed rations where appropriate. The May soybean meal contract closed at $291.8/ton on April 16, 2020 roughly $45 less than three weeks prior. The April WASDE report increased domestic soybean meal use 300,000 tons to 37.1 million tons, 2.7% above last years disappearance. With a national hog herd 4% larger than last March and a near record cattle on feed number elevated soybean meal for feed use seems likely to continue. One caution would be the announcement of pork and beef packing facilities either closing or slowing output as a result of COVID-19. Packing slowdowns decrease the demand for live animals and producers are forced to slow the rate of gain in animal growth and thus feed usage. However, if packing plants start reopening and moving toward full speed soon and ethanol production remains suppressed, putting a limit on DDG availability, it is possible to see increased feed use for both soybean meal and corn.

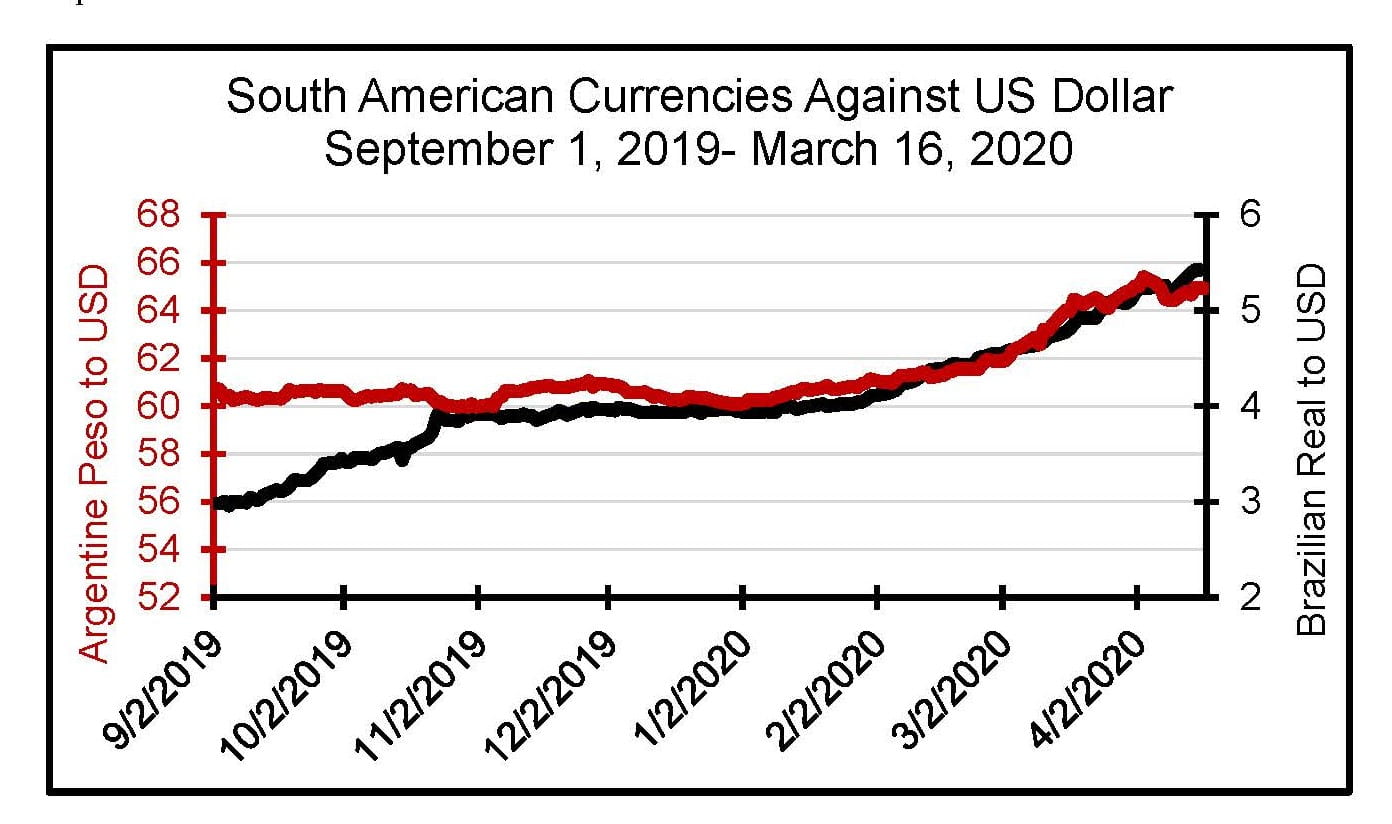

Strong soybean meal exports are also supporting increased crushing. The April WASDE report increased the forecasted value for exports during the marketing year to 250,000 tons. At 13.45 million tons the current marketing year will be 104,000 tons below the 2018/19 total after exports lagged heading into the start of the marketing year primary on strength of South American crushing and currency exchanges. The Peso has depreciated 32% against the Dollar since August 1, 2019 with a similar drop to the Real. Through the first seven months of the marketing year, soybean meal exports sit 4% below the same period last year and total commitments are 3% below the three-year average. However, this has improved from the weak sales and exports in November and December. Outstanding sales for the remainder of the marketing year are just over 2.7 million metric tons but remain 12% below the outstanding sales reported at this time last year. Increased exports to Canada and Central American are only partially making up for decreased sales to Vietnam (-63%), the European Union (-40%) and Japan (-56%). Unless COVID-19 continues to cause logistical challenges in Argentina it is difficult to see how the US maintains the strong export sales experienced in March. It is possible to see a reduction to 13.35 million tons of soybean meal exports.

Soybean oil prices have found a little strength on technical support in the last couple weeks after being on a steady decline since the start of the calendar year. Soybean prices started the year at just over 35 cents per pound before bottoming out mid-March at 25 cents per pound. This was the lowest value for soybean oil since October 16, 2006. Soybean oil import forecasts have been reduced for China, India and Venezuela on weaker economic activity and reduced competitiveness for biodiesel to gasoline. However, reduced production in Argentina due to COVID-19 did allow the US to pick up some soybean oil sales. Price competitive palm oil prices out of Indonesia are putting pressure on soybean oil exports. World stocks to use of oils at 6.3% is 1.3% less than a year ago on increased palm, soybean and sunflower use. Accumulative export sales through the first seven months of the year sit 40% above the same period a year ago, but sales also started out the year very strong. Total commitments for the year sit 28% above the three-year average with outstanding sales of roughly 309,000 metric tons which is 64% above a year ago with large sales to South Korea in March. Even with a reduction of 200 million pounds in the April WASDE, exports in 2019/20 are estimated to be almost 24% above last years oil exports. Given the strong export sales already this year it is likely that the US will exceed last years value, but lingering COVID-19 impacts on biodiesel and economic activity globally make maintaining the rapid export pace unlikely.

COVID-19 has put a damper on strong domestic use of soybean oil. Current estimates are for a 474 million pound reduction in domestic disappearance of soybean oil to 22.4 billion pounds. Lack of motor fuel use continues to put downward pressure on biofuels eroding the forecast as people stay home.

Summary: The March NOPA crush values shattered monthly crushing records on increased demand for both meal, strong oil exports and healthy crush margins for processors. Historical pace would imply 2019/20 soybean crush at 2.140 billion bushels, but infrastructure constraints and declining demand for soybean oil compared to March could dampen soybean crush through the remaining six months. USDA raised soybean crush 20 million bushels in the April WASDE to 2.125 billion. At this time that adjustment is justified, but we might not see a crush report like March for a while.